What does Bupa offer in terms of mental health cover?

Bupa is undoubtedly the best-known private health insurer in the UK, with more members than any other insurer. In this article, we'll focus on their mental health offering, explaining what's included, how it works, and why Bupa's mental health cover stands out.

Chris Steele founded myTribe and is a CII qualified insurance expert (IF1, IF7, I10) with over ten years of experience in private health insurance. His research is regularly cited by The Times, The Guardian, The Telegraph and other national media.

Full BioIntroduction to Bupa mental health cover

Bupa includes mental health cover as standard with their Bupa By You health insurance plans. Unlike most other insurers in the market, where mental health cover is an add-on, it comes with both their Treatment and Care and Comprehensive policies.

Bupa Treatment and Care: what mental health cover is included?

Treatment and Care is Bupa's entry-level health insurance plan designed to help once you've been diagnosed with a condition. In relation to mental health, you can access 28 days of inpatient or day-patient psychiatric care each year for each policy member. This means if you need to be admitted to a hospital after your mental health diagnosis, you'll be covered for a set amount of days.

Bupa Comprehensive: what mental health cover is included?

Bupa's Comprehensive cover offers the same level of in and day-patient psychiatric care as Treatment and Care. It also includes out-patient consultations with mental health specialists up to your chosen out-patient limit.

Bupa operates on a 'combined limit per person, per year' basis, meaning all out-patient services fall under one limit, with each person on the policy having their own individual limit. However, these limits don't apply if your out-patient care is for eligible cancer treatment.

Related guides:

Bupa offers cover for numerous mental health issues and disorders, stating on their website that they cover more conditions than any other UK insurer. These include:

- Acute stress reaction: Acute stress reaction is usually a sudden, short-term reaction to a life event, such as losing your job, bereavement, an accident or being a victim of crime.

- Adjustment disorder: Stressful life experiences can disrupt the normal adaptation process and bring on anxious feelings, worry, broken sleep, difficulty concentrating, fatigue and feelings of sadness and crying.

- Alcohol misuse: Alcohol misuse is when you're either dependent on alcohol or your drinking has become harmful to you or others around you.

- Anxiety: Anxiety is a natural reaction to specific situations; however, for some, it can spiral and become debilitating.

- Bipolar disorder: Bipolar disorder causes significant mood swings, often with periods of elation and hyperactivity and periods of depression.

- Dissociative disorder (conversion disorder): Dissociative disorder can be short-lived following a traumatic life event, or it can be a much longer term condition and is a range of conditions that can cause physical and psychological problems.

- Eating disorders: Anorexia, bulimia and other eating disorders are when you have an unhealthy attitude to food, which can cause physical and psychological harm.

- Mixed anxiety and depression: If you have equally balanced symptoms between these two conditions, you may be diagnosed with mixed anxiety and depression.

- Obsessive-compulsive disorder: Obsessive-compulsive disorder (OCD) can vary in severity from mild to extreme, and it causes people to think and act obsessively.

- Panic disorder: Panic disorder is categorised as recurrent panic attacks, where you have extreme fear or feelings of panic.

- Personality disorder: Personality disorders, including borderline and antisocial personality disorders, make people think and act differently than they usually would.

- Phobias: Phobias can be mild or severe and typically involve intense fears of an object or situation, such as a fear of eating in a restaurant or dogs.

- Post-traumatic stress disorder: Post-traumatic stress disorder (PTSD) is a psychological disturbance after an event, such as witnessing a horrific event, an accident or assault.

- Postnatal depression: Postnatal depression can affect women after they have given birth and is more serious than typical baby blues that many women experience in the first week or so after giving birth.

- Psychosis: Psychosis is where you interpret the world and events around you very differently from others.

- Recurrent depression: Depression can sometimes affect people just once, but others can experience recurrent depression where it's repeated.

- Schizophrenia: Schizophrenia typically involves delusions, disorganised thoughts, incoherent speech and unpredictable behaviour.

- Substance misuse: Substances such as drugs that alter your state of mind can lead to abuse, addiction and harm.

- Seasonal affective disorder: Seasonal affective disorder (SAD) is a type of depression which you typically experience during the winter when there is less natural sunlight.

- Schizoaffective disorder: Schizoaffective disorder is different to schizophrenia and bipolar, and it's where symptoms of both psychotic and mood disorders are present together.

A key feature included in both plans - and which is directly and indirectly related to mental health - is Bupa's addiction treatment programmes. These programmes support a range of addictions, including alcohol, drugs or gambling, with each policy member being eligible for one programme during the lifespan of your policy.

Useful link

In this guide we look at Bupa Private Health Insurance, explain the various options that you can choose from and highlight its standout features.

While Bupa covers many mental conditions, there are some exclusions to be aware of.

Treatment of and support for those suffering from Dementia are excluded from Bupa health insurance policies, which is the same with all health insurance companies in the UK. The primary reason for the exclusion is that all health insurance policies are there to help people get back to where they were following an acute illness. Unfortunately, dementia is typically a chronic condition that needs careful management.

Bupa also excludes learning, behavioural and developmental conditions such as Asperger, ADHD and dyslexia for similar reasons, in that they need long-term care and management, not short-term treatment.

What our health insurance expert says:

"If you have out-patient cover with Bupa, they will usually cover tests and consultations leading to a diagnosis of an excluded condition such as dementia and it's only once diagnosed you'd be expected to go back to the NHS or self-fund private treatment.The reason diagnosis will often be covered is until you've had tests, scans and specialist consultations, it's impossible to know whether the condition you have is something chronic, such as dementia, or potentially an acute illness which you could claim treatment for under your policy."

Are pre-existing conditions covered?

Pre-existing conditions are those that exist prior to applying for your policy. Most insurers - including Bupa - don't cover these conditions; instead, they base their cover on future health conditions that may arise.

Depending on which underwriting method you opt for, you may need to tell Bupa about any existing mental health conditions before taking out a policy. If you opt for moratorium underwriting, you won't need to tell Bupa about pre-existing mental health conditions, but anything you've suffered from in the past five years will be automatically excluded.

Remember, though - don't assume you're eligible to claim for these conditions just because your insurer hasn't asked about them; if you claim, your insurer will look into your medical history.

Exceptions to the rule on exclusions and pre-existing conditions

If you're unsure whether your policy covers your condition, speak to your insurer. Although they might state that a certain condition isn't covered, there may be exceptions, including covering you for conditions associated with your excluded condition. Here's an example that Bupa mentions on its website:

"If you've had PTSD before, we could still cover you for future unrelated episodes of stress."

Bupa offers members several ways to access care, from hands-on self-referral options to hassle-free guided pathways.

Bupa direct access

Bupa's Direct Access service lets you bypass your GP and receive certain mental health treatment without a referral. It's a phenomenal option if you're looking for immediate well-being support but don't have time to wait for GP appointments or referrals.

When using the service, you'll be connected with a trained mental health practitioner who will listen and help you understand your options. You'll have access to guidance and helpful resources; you may even be referred for online CBT (cognitive behavioural therapy), counselling or psychiatric consultation if required.

Open referral

Bupa also gives you access to care via open referral from your GP. This means that your GP chooses the type of specialist suited to your condition, and Bupa helps you find a relevant specialist covered by your policy.

Guided care

Bupa offers Guided Care as part of their open referral process - aiming to give customers a clear, affordable route to consultations, tests and treatments.

In choosing this option, you'll be given a choice of three Bupa-recognised consultants, selected based on your age and location. This approach aims to prevent the hassle of obtaining multiple referral letters if your first choice of consultant doesn't work out.

Opting for Guided Care usually reduces the cost of your premiums, as Bupa has more control over the specialists you'll see. If you want more freedom to choose your own specialist, you don't have to add Guided Care to your policy; just bear in mind this will likely increase your premiums.

Private healthcare insurers often have a network of hospitals and clinics that their customers can use should they require diagnosis, treatment or consultation. Bupa is no exception, building its network based on facilities with a reputation for high standards of care.

Hospital lists

Bupa offers three levels of network access; Essential Access, which includes a number of private facilities across the UK, with the exception of those in London. They also offer Extended Choice and Extended Choice with Central London, which are priced higher due to the location and reputation of their hospitals.

Unlike other insurers, Bupa lets you opt for both guided care and a hospital list if you wish, which means you know which hospitals you can use, and Bupa will recommend specialists at those should you need them. Other insurers typically bundle hospitals and specialists into their guided option, meaning they will tell you which hospitals you can use and the specialists too. In short, Bupa gives you more choice in this respect.

Bupa By You policies are packed with extras that add value to an already excellent package. But do these additions support customer well-being? Let's take a look.

24/7 HealthLine

All Bupa By You policy members can access its 24/7 Bupa Anytime HealthLine, giving you unlimited telephone consultations with Bupa's specialist team of nurses and GPs. This means if you need immediate support around your mental health and wellbeing, you don't have to wait.

To complement this service, you'll also have access to their Family Mental HealthLine, designed to support parents or carers of young people who are worried about their child's behavioural changes. As a bonus - your child doesn't need to be covered by the policy for you to receive guidance from Bupa's mental health advisers.

MyBupa

Smartphone users will find the MyBupa app a useful addition to their policy, giving them access to their policy details without needing to wait on the phone or log into a computer.

Where many insurers' digital services are limited in the actions you can perform, MyBupa lets you view your policy documents, search for ideal consultants and even manage your claims under one roof.

As part of the MyBupa app, you'll also have access to Bupa's Digital GP service, allowing you to attend or schedule free video or phone appointments with a mental health nurse.

Menopause Healthline

While menopause isn't a mental health condition, its symptoms have been shown to impact wellbeing. Bupa's Menopause Healthline allows policy members to access support and advice from specially trained nurses. Through this, they can discuss the impact of their conditions and explore options to support them in the future.

As mental health cover is included as standard in Bupa's health insurance policies, breaking down its cost is difficult. The cost of health insurance, however, hinges on a few variables, including age, location, lifestyle, the level of cover you select, and who you choose to include.

Our article titled 'How Much Does Bupa Health Insurance Cost?' explored this in detail, showing that the average Bupa health insurance policy costs around £82 per month. Our analysis was based on the typical health insurance buyer and included Comprehensive cover, with £1,000 out-patient cover and the Essential Hospital List.

Does it cost more to add mental health cover?

Most insurers offer a base policy with the choice to include additional options. Your basic policy starts at a set cost, increasing with each addition you make. Some providers include a base level of mental health cover, which can be increased at cost depending on your needs.

Bupa does things differently, offering mental health cover as part of their Bupa By You policies. This means you won't pay a penny extra for your mental health cover with Bupa.

Will claiming for mental health conditions affect my premium?

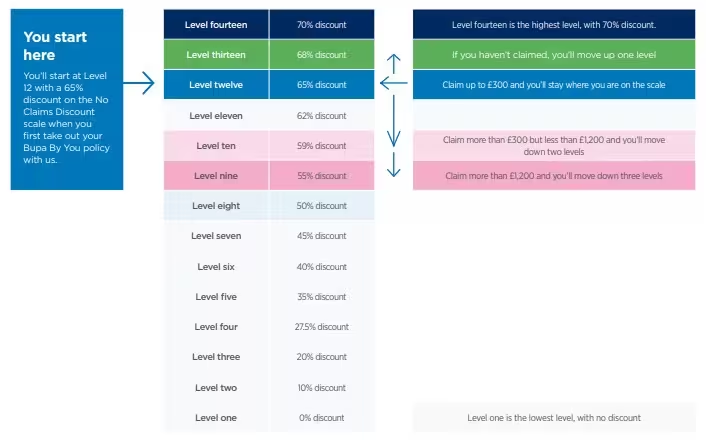

Making a claim will likely increase your policy's cost at renewal. This applies to all conditions covered on your plan, including mental health. With Bupa, the amount your policy increases each renewal is governed by their No Claims Discount (NCD) scale.

This scale helps Bupa calculate the cost of your policy by looking at the amount and value of claims made in the previous policy year. Bupa's scale comprises fourteen levels, with new policyholders starting at Level twelve, which gives them a 65% discount on their base premium.

Example: If you haven't claimed in the past policy year, you move up the NCD scale, resulting in a lower premium. However, if you have claimed a value of between £300-£1199, you would move down the scale by two levels, leading to a higher premium at renewal.

Right away, assuming it's for a condition that has come on after you took out the policy. You can claim for treatment as soon as your policy begins, but bear in mind that insurers will usually want to check you're not claiming for a pre-existing condition, especially if the claim happens very quickly after getting a policy. You'll also have access to Bupa's Anytime and Family Healthlines, should you require immediate support or guidance around your mental health.

If you're unsure of your policy start date, you'll find it in the welcome documentation you received after your application was approved. Failing that, you can find out more by contacting Bupa or logging into your policy portal.

Useful link

Discover average UK private health insurance costs from myTribe's analysis of over 12,000 quotes. See how age, postcode and cover level affect premiums in 2026.

In short, it is. Bupa health insurance policies offer a comprehensive approach that includes mental health cover as a standard. You don't have to worry about pricing up policy add-ons; apply and enjoy the benefits.

Pair this with a broad list of conditions and treatment options, plus Bupa’s commitment not to withdraw cover for long-term mental health needs, and you've got what we believe is the market-leading mental health cover in the UK.

Want to know more about Bupa health insurance? Read our in-depth Bupa health insurance review.

What our readers say

We're rated Excellent on Google from 160+ reviews. Reviews relate to the service provided by both myTribe and our broker partners.

Good support great knowledge caring empathetic and totally understanding

"The information was very helpful and informative. They put me in touch with an extremely helpful broker. I am now moving to a different provider, on a better policy, at a much reduced premium."

"Absolutely straightforward experience. The lesson? NEVER accept a renewal quote without shopping around!"

Disclaimer: This is general information, not personal advice. Speak to a qualified broker before making a decision. Our broker partners compare policies from a panel of leading UK health insurers, but not all insurers may be available.